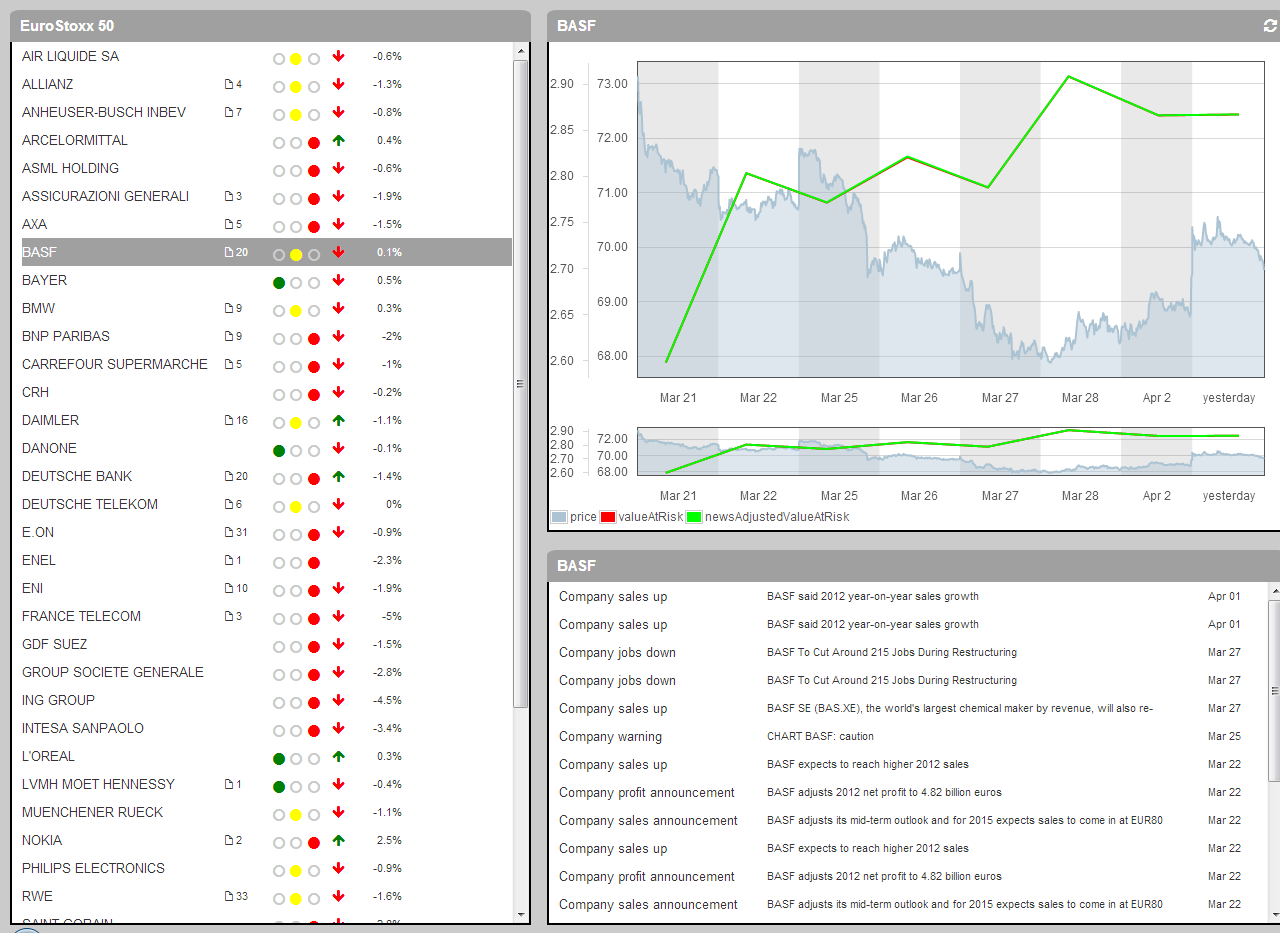

News adjusted Value at Risk improves traditional Value at Risk metrics by incorporating the semantics of breaking finance news.Financial news is commonly regarded as an important source of information. Multiple studies have shown that breaking news affects market volatility and therefore the risk involved in buying or selling stock.SemLab’s semantic processing of financial news extracts distinct news events which enables the development of a quantitative measure expressing the market risk resulting from breaking news stories. The underlying time series modelling is based on the GJR-GARCHX model in which we incorporate the news effects. It is developed in collaboration with Fraunhofer institute of Mathematics.We have developed a demonstrator application – the News adjusted Value at Risk viewer – which shows the live Value-at-Risk (VaR) and price development of the 50 leading equities (Euro Stoxx 50) of the Eurozone. It receives a continuous stream of financial events from our ViewerPro semantic analysis platform and tick data from Yahoo! Finance. From this data it automatically determines the News adjusted VaR and for comparison the 95% traditional VaR on a daily basis with a horizon of one year.All this data is conveniently displayed in an interactive chart. The viewer has the following features:

✩ a history of 2 weeks

✩ 50 leading equities of Europe (Euro Stoxx 50)

✩ the amount of news, a VaR traffic light, an arrow indicating the last price change and the daily return per equity

✩ ViewerPro news events with an excerpt from the originating news item

✩ a price chart

✩ Value-at-Risk chart (both Traditional and News adjusted)

✩ the chart supports zooming by selecting a duration in its bottom section.