Financial news is commonly regarded as an important source of information by equity traders. The reason for this is that the news may contain previously unknown information that may affect the fundamental value of a company. News containing information that indicates a higher value is called “positive news”, as opposed to “negative news” indicating a decrease in fundamental value.

Once a trader decides to trade, the price of a share in the affected company will change, leaving traders that were unaware of the information at a loss.

The extent of the effect of news messages on equity prices is a popular research topic in recent economic science. Most authors agree on an increase in liquidity (both volume and volatility) following a publication in the financial news. However, conclusions on its effect on equity prices are less clear. Most authors recognize that the news effect is one of many socio-economical factors affecting the equity prices and accept that its effect may not always be prevailing.

Strategy

One of the strategies to address this fact is to define criteria for what news messages are more likely to result in a equity price change than others, or inversely, what equities can be expected to be more susceptible to their coverage in the news. One of these criteria is the level of “unexpectedness” or “surprise” value of a news message.

It is evident that information that is common knowledge will not influence the price of any equity. Similarly, news that was either partly or wholly anticipated by market participants can be expected to have much less effect than completely unanticipated news.

One way to model the surprise value of an event reported in a financial news message is to compare its directional bias (either positive or negative) with the recent technical sentiment of an equity. News with a positive bias for a bearish stock is more surprising than for a bullish one and vice versa.

Result

This strategy was implemented on a historical dataset of about half a year daily return data of the Stoxx50. ViewerPro was used to detect the common financial events associated with these equities that were reported in the popular newswire services during this period, resulting in over 46 thousand event occurrences.

The technical sentiment of the stock was determined by a voting engine consisting of Simple Moving Average, Exponential Moving Average, Bollinger band and Rate of Change indicators of the stock price over the 20 days preceding the event. The stock prices were corrected for the behaviour of the index.

The return was determined to be the difference between the closing price of the day preceding the event and the closing price of the stock on the day that the event occurred.

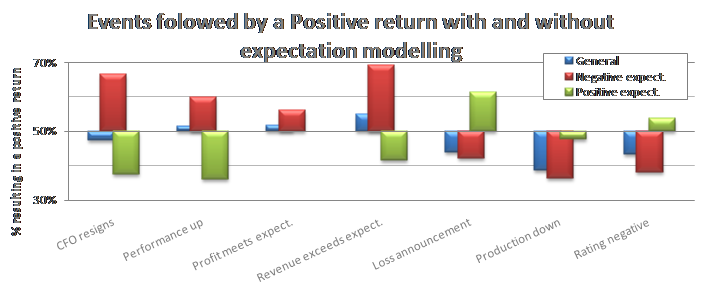

Using this implementation, a striking difference was found between the returns associated with event occurrence during positive or negative expectations and the returns without expectation modelling. For example the event “Revenue exceeds expectation” was found to correlate with a positive return in 69% of the cases during a negative expectation, compared to just 55% without expectation modelling. (Note: 50% is the expected value of any event since the expectation is either positive or negative).

Conclusion

This implementation illustrates the potential benefits of using financial news to improve returns when trading on unexpected events. Depending on the event type, an improvement of market direction prediction of up to 19% can be made by using a combination of market sentiment and events from financial news messages.

If you have any questions about this section or about using ViewerPro semantic processing and data extraction in general , please contact us for a free demo of our software.